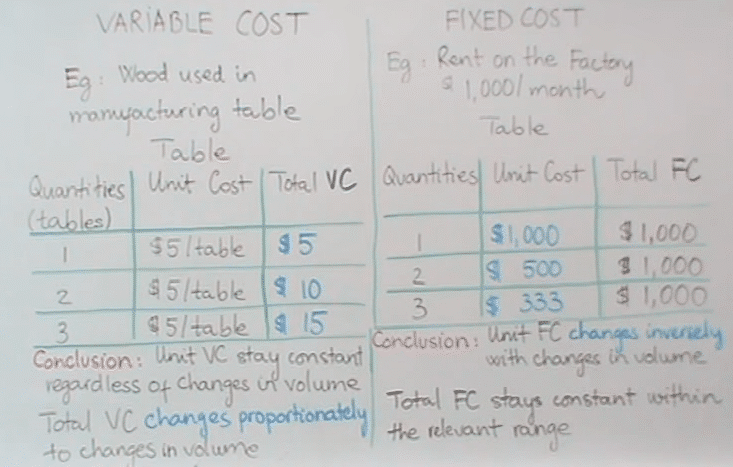

Variable cost

OK, let's start the discussion with variable costs. Assume that we are going to be manufacturing tables.

Let's assume that we are going to use wood to manufacture our tables. So wood would be a raw material that's used in the manufacture of our tables.

Let's assume that each table requires five dollars of wood. So based on this information, let's go to the table that I have prepared for you here.

If we manufacture one table, the unit variable cost that is the amount of wood per unit table would be five dollars, and the total wood cost for one table will also be five dollars. But look what happens when we go and manufacture two tables.

When we manufacture two tables, the amount of wood used per table is still five, so our unit variable cost stays constant, does not change at five dollars a table.

But look at what happens to the total wood cost, the total variable cost when we manufactured two tables. The total wood cost now has changed to ten dollars from the earlier five.

Let's go down with three tables. When we manufacture three tables. Again the amount of wood per table does not change that stays the same at five dollars per table, so your unit variable cost stays constant at five dollars.

But look at the total wood cost. The total wood cost now has gone up to fifteen dollars.

So what conclusions can we draw from this table. The conclusions are that your unit variable cost stays constant with changes in volume. But your total variable cost changes with changes in volume.

If your volume goes up, your total variable cost goes up. If your volume drops, then your total variable cost comes down.

So wood is an example of a variable cost, and I have just illustrated that behavior pattern of both unit variable costs as well as total variable costs.

Now one of the assumptions we make here is that there are no volume discounts granted for large volume purchases, so that's the assumption we make. So whether we buy, you know, small amount of wood or whether we buy a large amount of wood, we are going to continue paying the same amount for each square foot of wood. So that's the assumption here no discounts given for volume purchases.

Fixed cost

OK, let's pay attention now to fixed cost. So if we assume that the fixed cost we have is rent, rent of $1,000 a month. Again let's assume we will be paying a rent of $1,000 a month. So if we have to pay rent at $1,000 a month, let's see what would be the behavior pattern of unit fixed costs and total fixed costs as we change the volume of tables manufactured.

So when we manufacture one table, the total rent I pay my landlord is $1,000, because my landlord does not care whether I make one tables or 10 tables. He still wants his $1,000. But If I want to take that total $1,000, and allocated among the tables manufactured which in this case is only one table then one single table gets allocated the entire $1,000 of rent. So my unit fixed cost also in this case is $1,000.

But look what happens when we go to two tables. When I manufacture two tables, my landlord still wants his $1,000 of rent, doesn't he? So my total rent fixed costs still stays the same at 1,000. But when I go to allocate the $1,000 among the two tables I have manufactured, then this time each table picks up only $500 as $1,000 over two picks up only $500 of rent.

So when unit fixed cost is dropped from $1,000 per table to $500 per table. But my total rent cost has stayed constant at $1,000 regardless of where they manufactured one table, two table or three tables. So when I manufacture three tables again, my landlord still wants the same $1,000 of rent. So my total fixed cost at three tables still remains constant at $1,000

But look what happens to my unit fixed cost, that is when I take the $1,000 of rent and I allocated over the three tables that I manufactured, each table now picks up only $333 of rent as opposed to the $500 earlier and the $1,000 before that.

So what conclusions can we draw about the behavior patterns of fixed costs from this example. Your unit fixed cost changes inversely with changes in volume. It was a $1,000 first, then 500 then 333. But look at your total fixed cost as I said before and I repeat your total fixed cost does not change with changes in volume stays the same as well within a relevant range.

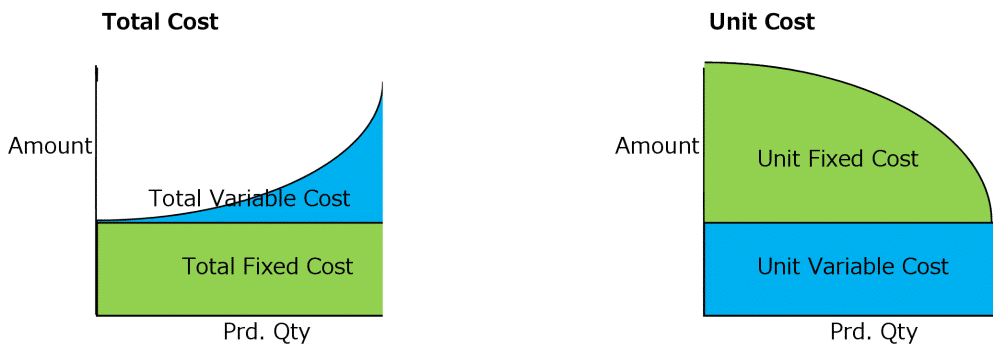

Total cost and Unit cost

Now I introduce a new concept, your new term, relevant range. What do I mean by the term relevant range? In this case let's assume for instance that if I were to operate my factory 24/7 three shifts a day, let's assume I could manufacture a maximum of 10,000 units. So in this case we would say in this example the relevant range is between one unit and 10,000 units.

What does that mean? That means what we are saying is that my total fixed cost of $1,000 will stay at 1,000 regardless of whether I manufacture one table over there manufacture 10,000 tables. So as long as I stay within the relevant range, my total fixed cost of $1,000 stays at 1,000.

But If I want to manufacture more than 10,000 tables, I would have to probably rent another building and pay another $1,000. In that case if I went over 10,000 units of manufacture, then my fixed cost would increase, would go pass the 1,000, because I'm going outside of my relevant range. So that's a little bit about the concept of relevant range.

Now let's take these two items that we have talked about, and look at the effect on your total cost. So if you look up here on this part of the whiteboard, your total cost is equal to your total fixed cost plus your total variable cost.

We can express the same equation on a unit cost basis, so my unit total cost will be equal to my unit fixed cost plus my unit variable cost.

So let's look at this table to understand the effect of fixed costs and variable cost on my total unit cost. So if I were to manufacture one table, from our previous tables my unit fixed cost is $1,000, my unit variable cost is $5, so my total unit cost is $1,005. It's combining the two.

But look what happens to my total unit cost when I manufactured two tables. Now my unit fixed cost again from the previous tables is 500, my unit variable cost stays the same at $5. So this time my total unit cost has dropped from 1,005 to 505, lot cheaper to make two tables than to make one table.

And see how that unit cost drops when we make three tables, going to make three tables. What happens to my unit fixed cost we get from the previous tables is down to 333. My unit variable cost does not change, it stays the same at $5, so now total unit cost is only $338.